Let's Get Right To It

In this blog post we are going to walk through (and defend, maybe?) all the different EBITDA adjustments in the schedule below:

The Purpose of EBITDA

EBITDA is a calculation designed to show us the normalized estimate of the profitability of a business (and also an approximation of operating cash flow) by removing:

- Differences in Financing Structure (Interest)

- Differences in Corporate Structure (Taxes)

- Differences in Accounting Polices (Depreciation & Amortization)

- Non-recurring Revenue or Expenses

These items are often called "adjustments" or "add-backs."

We do this because EBITDA is commonly used as a basis for business valuation, and the normalization makes the company comparable to others.

That's it. That's the point.

Normalized profitability for the purposes of valuation.

Mind the GAAP

Perhaps most fun and why EBITDA is such a polarizing topic is because EBITDA is not part of GAAP. It's a glorified Finance arts and crafts project.

So when it comes to the non-recurring Revenue and Expense items I mentioned above, Management is free to include (or exclude) whatever adjustments it wants.

Accordingly, it's on the buyer to scrutinize these adjustments in detail to ensure the normalized profitability is accurate.

Where might you find a schedule like this? Normally in a financial model, one-off analysis, or more formally in a Quality of Earnings ("QofE") report.

From the Top

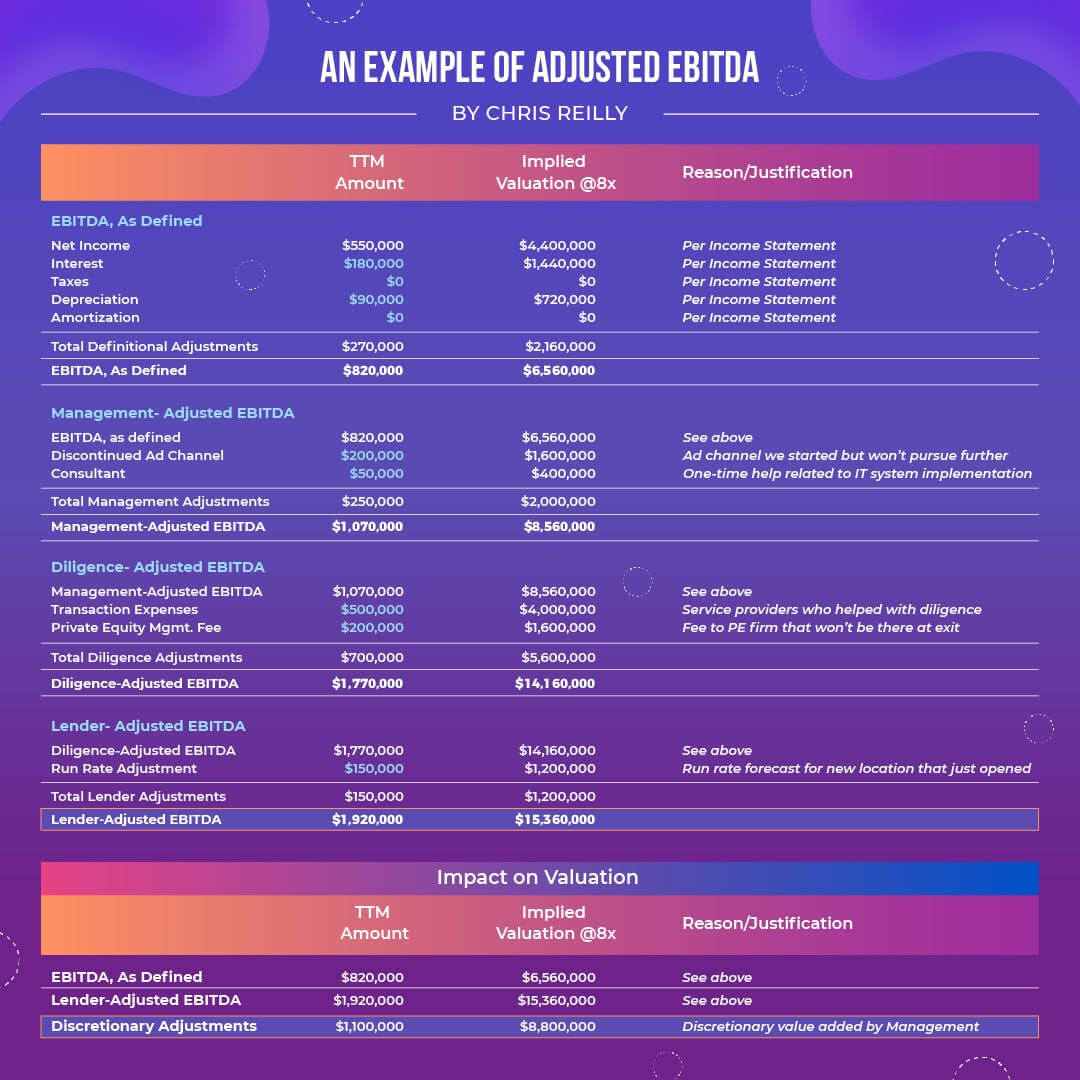

EBITDA, As Defined

Net Income

We start with Net Income, and that's easy enough: it's the "profit" or "earnings" of the company after all.

But like I said at the start: companies do things differently, so we need to compare by removing the impact of:

- Differences in Financing Structure (Interest)

- Differences in Corporate Structure (Taxes)

- Differences in Accounting Policies (Depreciation & Amortization)

(all stuff that could potentially change)

So here's what we do...

Interest

A little tricky... we add this back because a company could be purchased with all equity and wouldn't need any debt, and therefore wouldn't have Interest Expense.

So we "add-back" the Interest Expense to show what it would look like "debt free" and effectively normalize the financing structure.

Taxes

Don't we all have to pay taxes? So why add this back?

It all comes down to the business structure.

There are several business structures known as pass-through entities, meaning there is no "corporate income tax." Rather, the taxes are "passed through" the business and end up on the personal returns of the members.

Typical pass-through entities would be S Corps, Sole Proprietorships, LLCs, and Partnerships.

The structure that is not a pass-through is a C Corporation. This type of business would show an income tax expense on it's income statement (whereas the other types would not).

So, that's why Taxes get added-back -- we are showing a "tax-neutral" view of the business knowing that its business structure could change as part of an acquisition.

💡In addition, all other adjustments mentioned throughout this article (Interest, Depreciation, Amortization, and Discretionary Adjustments) are all expenses that affect tax, so as expenses are removed, the taxes would change as well. So we need to strip them out.

Depreciation & Amortization

Companies can choose to Depreciate things differently (i.e., Straight-Line vs. Declining Balance method).

So we "add-back" these expenses to Net Income to normalize any differences in Accounting Policy.

In addition, these are non-cash expenses, so these adjustments help solve the secondary part of the EBITDA exercise, which is building an approximate operating cash flow.

EBITDA, As Defined

It's called "As Defined" because we've addressed the literal components of the abbreviation "EBITDA." EBITDA As Defined is usually a figure people can agree on (as a starting point).

Management-Adjusted EBITDA

Now we get into the "arts and crafts" portion of the schedule, because from here on out we're looking at discretionary adjustments or "add-backs" made by the Management team.

Discontinued Ad Channel

Management says:

"We tried out this Ad Channel but it ended up not being profitable. We won't use it again, so we're adding it back to illustrate that the expense won't exist in the future."

Buyer says:

"Okay, fair enough, but will you pursue a different Ad Channel going forward? If so, we should reflect that cost in our diligence adjustments or perhaps remove credit for this add-back. However, if it's truly one-time in nature, we're okay keeping it in the schedule."

Consultant

Management says:

"We hired a Consultant to help us with some Financial Modeling but won't need their help going forward, so we're adding back their cost."

Buyer says:

"Has the Consultant been replaced with someone working full-time? What is the difference between the cost of the Consultant and the employee? We're okay adding back the difference in cost, but not the entire thing. However, if the responsibilities of the Consultant have been fully absorbed by the existing staff, we're okay keeping the full amount in the schedule."

Management-Adjusted EBITDA

You can see how this is an ongoing negotiation between buyer and seller as to what is truly one-time in nature versus recurring. In a real transaction there will be several of these "management adjustments."

Diligence-Adjusted EBITDA

Oddly enough, these are often easier to defend than the management adjustments because they're less discretionary in nature. I'll explain...

Transaction Expenses

These are definitely one-time in nature. These costs represent Lawyers, Accountants, and other service providers that assist with diligence to help get the deal closed, but they won't be recurring costs going forward. Therefore, they are easy to justify on an add-back schedule.

Private Equity Management Fee

This one is a little trickier because you could argue that the Private Equity firm brings an ongoing value to the company that would need to be replaced once the firm "exists" (sells) the company.

However, typically the Private Equity firm will say "this is just a temporary cost to help compensate us for our time, but won't exist when we sell the company down the road."

Lender-Adjusted EBITDA

Now we're back to getting "creative," and Private Equity firms are pros at this.

Run Rate Adjustment

Forget historicals (like Management Adjustments), now we're talking future!

The company might say, "we just opened a new location and it's only been a month.

However, this is our 7th location and we're fairly confident it will generate $150,000 in EBITDA, so we'd like full 12-month-credit for it now."

Sounds a little whacky at first, but then again, it is their seventh location, so maybe it's reasonable?

I've seen a few responses from lenders on this:

- No way, it's in the future and we'll give you credit once actuals come in.

- Fair enough! You can have full credit for it now.

- We'll give you full credit for actuals, and 70% credit for your forecast.

Why even have this? It helps the company stay in covenant compliance earlier on, as the Fixed Charge Coverage Ratio and Leverage Ratios often refer to Adjusted EBITDA.

In the end, it's contingent upon the situation and the relationship with the lender.

Impact on Valuation

Remember the purpose here -- normalization of profitability.

However, as we've discussed, the adjustments are discretionary (arts & crafts), so that's why the adjustments are so heavily scrutinized.

You can see in the image above that the company has proposed $1,100,000 in adjustments, which increases the valuation by $8,800,000 assuming a multiple of 8.0x.

That's the "power" of each of these adjustments -- each $1.00 adjustment is worth $8.00 of valuation.

What's reasonable? What's not?

That's for you and your team to decide.

That's it for today. See you next time.

—Chris

Did you know...

When I worked in Private Equity, the Managing Partners were obsessed with EBITDA. In fact, as an Associate, if I didn't know what EBITDA was for our portfolio companies, you can bet I heard about it later.

Don't get caught like a deer in the headlights during your Monday meeting, sign up for my Financial Modeling courses today and see exactly how to build this schedule and use it for valuation.

"⭐⭐⭐⭐⭐...I've learned more from Chris' courses than from countless free YouTube Videos and several paid big name courses. If you're wondering whether to buy the course, don't hesitate."